Investing in Startups at AI's Point of Recursion (Part 1)

- A recent blog by John Spindler, General Partner of Twin Path Ventures -

Investing in startups today can become a binary decision based on whether you believe that AI will keep on improving and reach the so-called “recursion point” or if you believe it is an over-hyped bubble, about to burst and we fundamentally can go back to how it was before 2022.

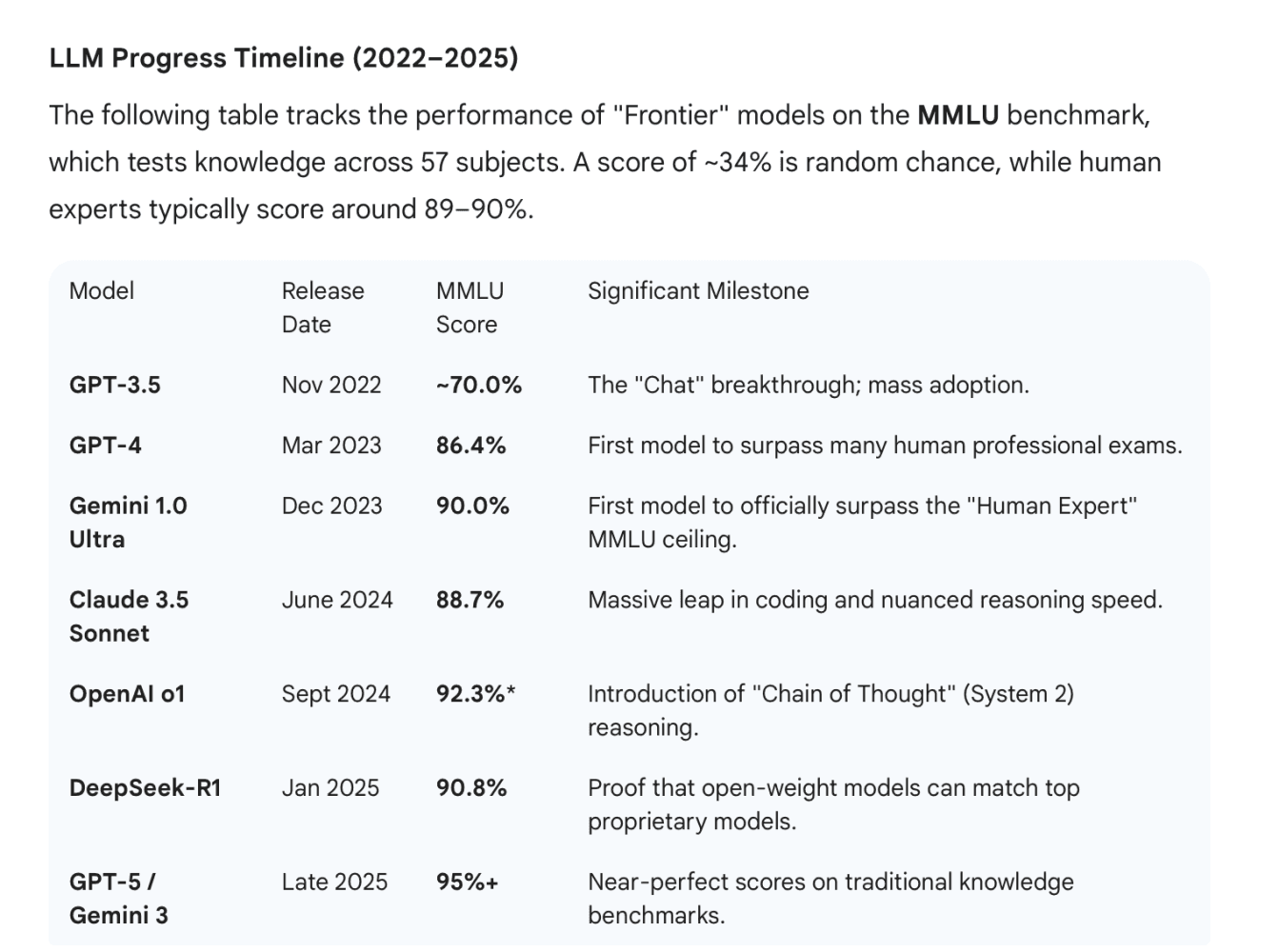

At Twin Path Ventures we think there is strong evidence that the progress in AI (especially but not exclusively AI that uses the scalable performance of LLMs) will if anything speed up in the next 2 years. Below is a timeline of improvement but if you want a more detailed and fun take check out this blog from Samuel Albanie and Andrej Kapathys end of year piece.

We concur with the observation made last month by Eric Schmidt Ex- Ceo of Google

“The San Francisco consensus is that at some point that stuff comes together and you get what is called, technically, recursive self-improvement. And recursive self-improvement is when it's learning on its own. This is not true today. Today when you set up one of these huge data centers - you know what they look like - you have to tell it what to learn. But the belief is that this is coming, and there's lots of evidence that this is coming. The ability for computers to write programs, to generate mathematical conjectures, to discover new facts, looks like it's very very close. Many people believe that there will be new math design, new mathematicians, Al mathematicians in the next year. So we collectively as an industry believe that this is going to happen soon. If you ask the San Francisco people, they'll say two years. Which is really soon. If you ask me, I double that to four years. Which is really soon. Right? So, it's happening. It's happening very quickly.'

We think that AI that is super-intelligent on many, if not the majority, of cognitive tasks that the best humans excel on is going to happen soon and when it does it will have a massive impact on the world, on industries and particularly startups that cannot shelter behind well established brands or scaled physical manufacture and distribution (and not-forgetting these assets will also be transformed by super-intelligent AI applications generating new winners and losers).

For some investors (and a lot of startup founders) it would be more than nice to go back to the world they knew pre- Chat GPT 3.5, to have faith that the recursion point for AI is not close. For those investors, the temptation must be to head back to the well trodden entrepreneur roadmaps and SaaS napkins, the trusted and proven milestones and rule of 40 benchmarks. The comfort of a recent past, when an investor seemingly had the ability and data to find out the fundamentals to set/calculate the valuation of a startup, stock or share price at time T1 and then be confident based on that baseline that they can predict and calculate where the valuation would be at Time T2, and consequently price the arbitrage opportunity. Heady days.

For VCs the wonderful ability when investing in SaaS startups/ scale-ups, pre 2022, to reliably use CCA/LTV ratios, a few months/years of a historical MoM growth record, received wisdom on market size and dynamics and industry price comparable multiples to make calculated investment decisions. All this data, then available for Series A+ investor, so they can expertly calculate the amount of capital needed to fund the burn period required by a start-up to achieve substantial market share and eventual FCF generation point. A reasonable valuation today and the expected big valuation uplift tomorrow if everything goes to plan, discounted against the risk and price of capital. Bing, Bing, Bang and fingers crossed the startup you have now invested in will be one of the winners and … Repeat 5,10,20, 30 times when building a VC portfolio and hope the power-law kicks in. These were the funds to invest in and back. Heady days

Whilst SaaS valuations, for over 10 years, seemingly scaled linearly with revenues, AI startups do not. These startups are valued on a "zero or hero" basis; a technical breakthrough or a unique data moat can cause a 10x jump in valuation overnight but on the flip side can equally collapse on bad news just as fast. SaaS is "build once, sell many," while AI is "build once, pay every time you use it."

For numerous reasons including

lower gross margins (due to inference cost of serving models),

higher R&D spend needed to develop/fine tune models and integrate them into workflows,

the aim ( not always achieved) that an AI business model is to be paid for not by creating efficiencies for customers in their software spend but from replacing labour costs

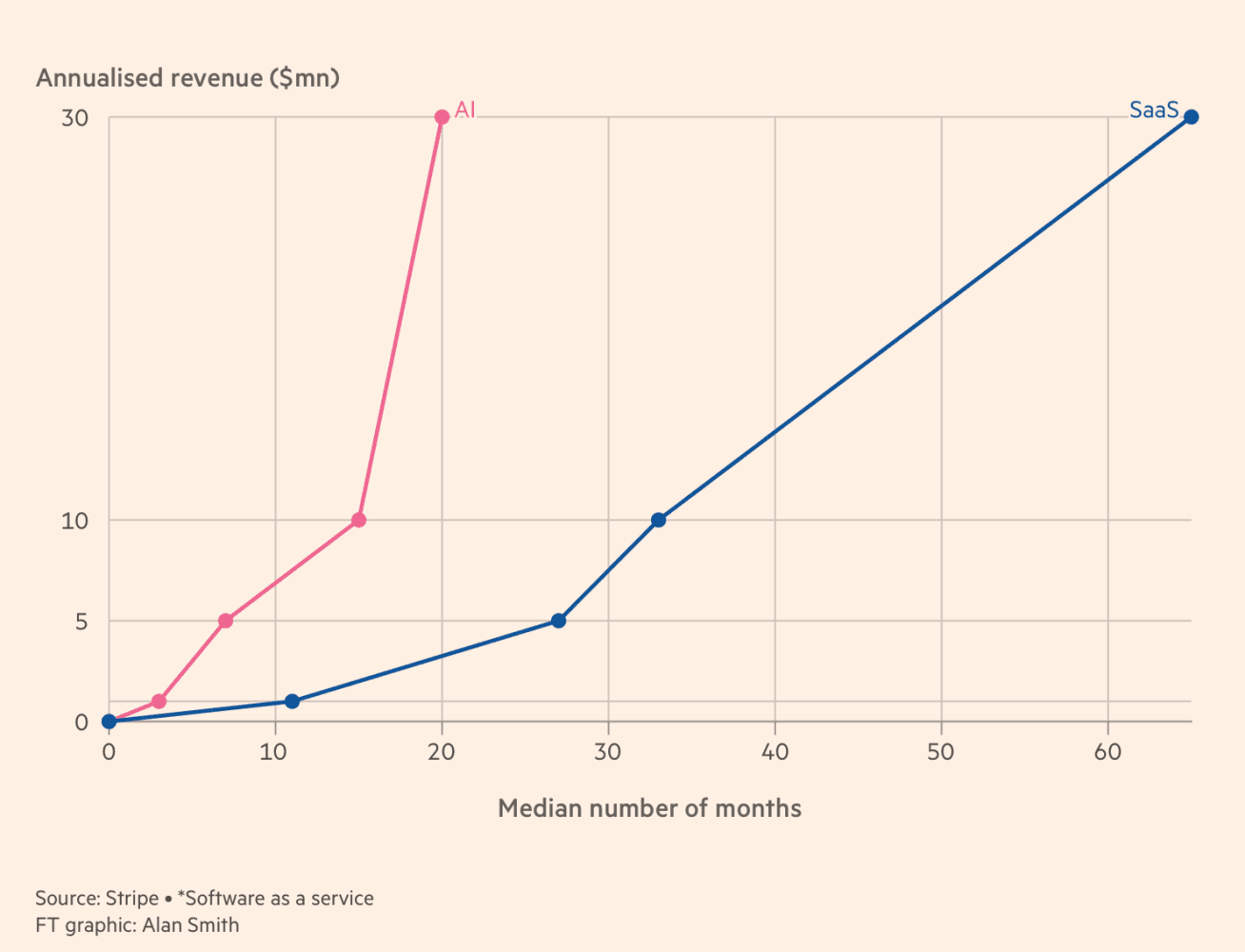

means that AI first startups are significantly different from SaaS. The benchmarks to evaluate potential, run comparisons and to estimate valuation are evolving and definitely not settled by the VC industry. As the FT reported, research from Stripe seems to show AI first startups scale faster (5x faster than the best SaaS scale-ups) but the cash burn to achieve that growth is most likely also significantly higher. So the roadmap followed by startups and the runway funded by VC’s needed to achieve the point of generating free cashflow that will “eventually” be needed to self fund growth is more difficult to forecast.

At the same time the sheer significance and speed of improvements in LLM models means a startup, scaleup and big incumbents software stack, especially their AI stack, can become obsolete overnight. [To date Twin Path Ventures believe that the only hedge against the risk of obsolescence that this R&D dynamism is producing, and thereby the prime signal of defensibility ,is the quality of the startups team's in-house AI scientists, data engineers and software architects and the speed and success of the team's “research-experiment- evaluate-deploy” iterative R&D feedback cycle. This we think will still pertain when the Recursion Point for AI occurs.]

What we are more confident of predicting is that the world of investing in startups through SaaS benchmarks and linear predictions is probably now on its way out because of AI and the revolution it is bringing. This is an uncomfortable position for investors, analysts and on-line commentators ( as well as founders). Prior to 2022 the crazies were early pre-seed/ seed investors (who without any or little data from the startup or the market needed to make a viable prediction model), were forced to invest on signals, promises and unproven thesis of startup founders. Now every investor is facing the possibility that they too might be “a crazy” as AI threatens to wash away incumbent markets, tried and tested business models, the previous benchmarks and prior growth expectations and all previous knowledge around data driven investing. Today a Series C startup, perhaps even listed companies, might be even more vulnerable to the AI tidal wave of change than a pre-seed startup. Backing the arbitrage between values at Time T1 and the value at time T2 seems more presumptuous than ever before.

So what do you do? Well there seems to be a few options investors are latching on to. These include:

Ignore it- carry on as before afterall is it not a bubble- is it not all over-hyped. Normal times will return. Probably the most fun and data driven case for the bubble thesis is Ed Zitron’s. Worth reading his blog. For what its worth I think he may be right on the bubble in regards to AI infrastructure investment ( here is Ethan Choi’s alternative take) and I think he is certainly right that the present business models of the foundational models, and AI wrappers built upon them, are unsustainable. They should be charging much, much more ( which they are starting too) because I think Ed Zitron is fundamentally wrong on the ability and impact of SOTA AI. But if you think otherwise, if you think the use cases are trivial, the size of opportunity is consequently small then lets judge everything by SaaS metrics or by linear growth and profitability metrics. Go for it.

Back the hype - many investors are momentum investors that jump from one wave to another as long as they have the knack of knowing when to cash in their winnings and jump off the peak before the inevitable correction. Many investors, especially those in public markets, are now looking to jump off the wave and invest in non- AI related stocks as a hedge against a market correction. Others are doubling down by exclusively investing on the early winners that are capturing new market share (regardless whether they are anything more than a wrapper on a LLM) or just showing the founding team's ability to raise big, particularly from Triple A investors. It kind of makes sense if you feel that brand, distribution and a lot of cash is what is needed to ride out a coming market correction. In consequence traction, especially big but super soft early revenue or prior big raises ( preferably both) has become the most important investment trigger for a Series A and beyond for momentum investors until… sentiment shifts and then almost overnight it is not.

3. Diversify away from AI - looking for sectors and (companies in that sector), immune to the impact of this generation of transformer model based highly scalable AI. A more deliberate strategy led by value ( as opposed to momentum) investors the primary challenge will be finding AI free startups when the number of niche sectors immune to AI disruption is rapidly diminishing. There are opportunities to invest in novel and innovative hardware/physical products and tradable assets. Before the emergence of LLM foundational AI, investing to solve real world logistical and infrastructure problems were all the rage. The time to build era of VC that attracted a lot of money to tackle the climate crisis, or the massive covid-era influx of funding to bio-techs or less successful, the splurge of money for last mile delivery or alternative city mobility. A lot of these issues remain but even here the impact of AI in reducing both the discovery and production costs, meaning that AI first startups are not just infringing on this world but driving innovation and disruption.

We at Twin Path Ventures are not following any of these strategies. We know for very good reasons there is a race in AI to hit Recursion or various“Recursion Points”. This is when AI becomes intelligent enough to autonomously & repeatedly improve on its own capabilities. Otherwise known as Recursive Self-Improvement (RSI) - recursing on its own capabilities to carry out specific tasks with each self-improvement cycle getting faster and faster to reach a super-intelligence that matches and surpasses humans. Big tech is desperately trying to achieve dominance in this race. So how does a pre-seed/ seed stage fund find, select and invest in startups that can compete in this race.

Twin Path has been thinking hard about this and the upshot is a revision of our investment strategy. Going forward we now believe that we have to take the coming Recursion Point seriously, and as such, invest in AI first startups built by world class AI scientists and engineers that can play a significant part in the race to recursion, or will be in a position to exploit the emergence of RSI when it happens or can have a defense strategy against big tech if they get their first or can explore the new AI frontiers where big tech are not.

What if RSI is about to be achieved in the next 2-4 years and super-intelligence becomes available on tap via a web app or an API call down. What then for knowledge work both by high-end professionals and middle-low end service providers. How do you prepare for this, how do you hedge your investments. Is it presumptuous to say that you should be investing in and/or with a fund that believes it can find potentially great startups and find amazing value in this market. We might be crazy to believe that the Recursion Point for AI is close but we may be right. What then for your investments and your present and future wealth. Can investing in Twin Path latest fund be your hedge?

Interested in learning more?

We launched Twin Path Ventures in July 2023 and to date, across 3 annual funds, we have invested over £30m in 36 pre-seed/ seed stage AI First startups. We intend to invest in more and invest in follow-on rounds of our winners. To reveal more about the details of our revised thesis on what to invest in when close to the point of recursion in AI, we are hosting an event on the evening of February 10th to launch our 26-27 Fund . Our fund, backed by the British Business Bank and some leading UK family offices, also offers the opportunity from HNW’s and Self-Certified Sophisticated Investors to invest through SEIS and EIS into AI-first startups for the 26/27 financial year.

Note: This event is strictly for High Net Worth or Self-Certified Sophisticated investors who meet the criteria for elective professional client status. Post registration, we will need to verify your status prior to attendance or on the night of the event.